FinTake Weekly: Markets Rally, Bonds Warn, and Oil Stays in the Spotlight

FinTake Weekly reviews global, GCC, Bahrain, commodities, and crypto market trends for the week ending May 23, 2026.

The week of May 17–23, 2026 delivered a familiar message: equity markets stayed optimistic, but the bond market, oil prices, and inflation expectations reminded investors that risks have not disappeared. Markets ended the week on a stronger note, supported by improving risk appetite, but investors remained cautious as higher bond yields, oil price volatility, inflation risks, and Gulf market sentiment continued to shape decision-making.

Global Markets: Risk Appetite Improved, But Not Without Warnings

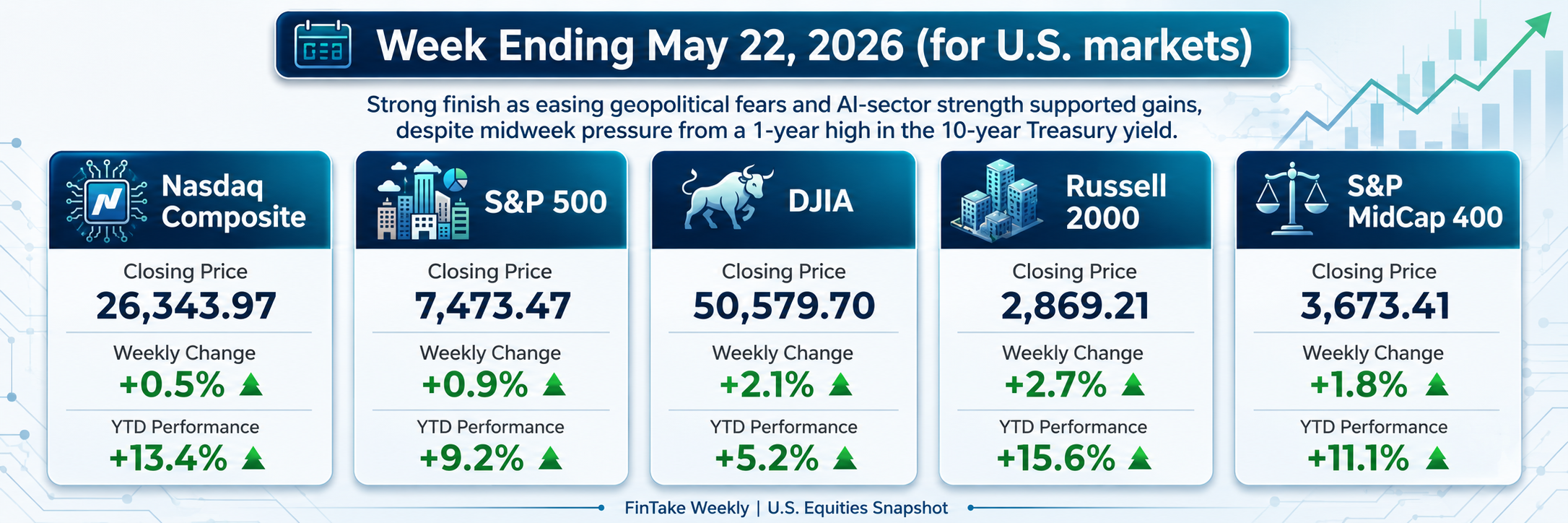

U.S. equities finished the week on a strong note. The S&P 500 recorded its eighth straight weekly gain, supported by easing geopolitical fears, AI-sector strength, and improved sentiment before the Memorial Day holiday weekend. The Dow also moved higher into the weekend, with reports showing it gained 294 points on Friday, May 22, reaching a new record high.

Still, the rally was not smooth. Earlier in the week, the Nasdaq and S&P 500 came under pressure as the 10-year Treasury yield reached its highest level in a year, showing that investors remained sensitive to higher borrowing costs.

Figure 1: US Market Performance — Week Ending May 22, 2026

Gulf Markets: Sentiment Improved on Iran Deal Hopes

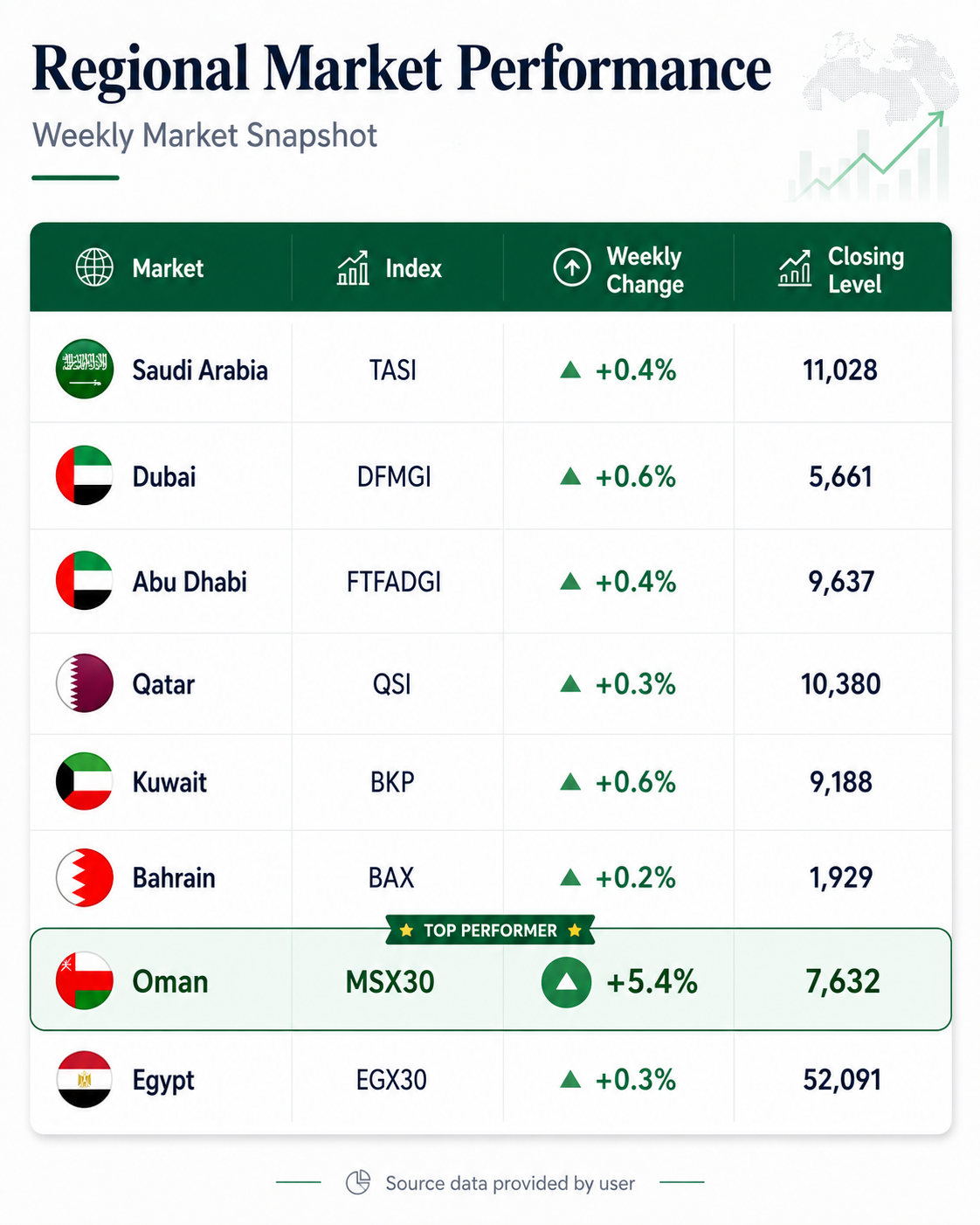

Gulf equities also reacted to geopolitical headlines. Reuters reported that GCC markets closed the week on a broadly positive note, with all major indices recording gains. Oman was the clear standout performer, as the MSX30 advanced 5.4% to 7,632, far ahead of the rest of the region. Dubai and Kuwait also showed solid momentum, each gaining 0.6%, while Saudi Arabia and Abu Dhabi rose 0.4%. Qatar and Egypt posted modest gains of 0.3%, and Bahrain added 0.2%.

Overall, the data reflect steady investor sentiment across GCC and regional markets, supported by broad-based but uneven upward movement.

Figure 2: Weekly Performance Across Major GCC Markets

This shows that regional investors are watching two key variables closely: whether oil routes remain secure and whether geopolitical risk continues to decline.

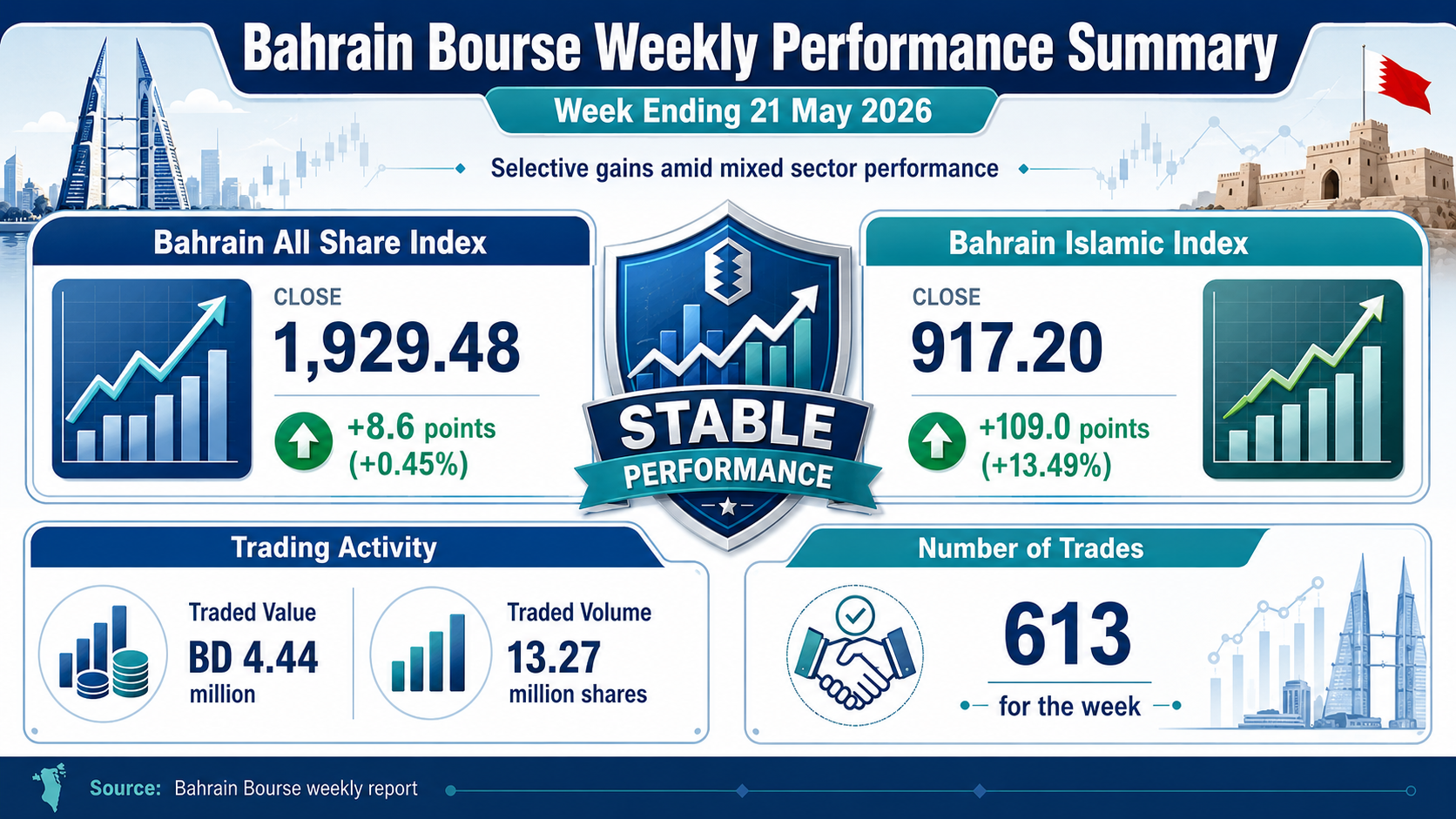

Bahrain Bourse Weekly Market Review

Bahrain Bourse closed the week ending 21 May 2026 on a mildly positive note, with the Bahrain All Share Index rising 0.45%, moving from 1,920.84 to 1,929.48. The broader market showed selective strength, although trading activity softened, with total traded value at BD 4.44 million, traded volume at 13.27 million shares, and 613 trades recorded during the week.

The Bahrain Islamic Index delivered a stronger performance, rising 13.49% from 808.21 to 917.20, making it the standout index for the week. Among individual stocks, NHOTEL led the weekly gainers with a 3.70% increase, followed by BBK, which gained 2.39%, and NBB, which added 0.40%. On the losing side, SEEF fell 6.80%, UGIC declined 2.94%, and KFH dropped 2.16%.

Figure 3: Bahrain Market Indices Summary

Sector performance was mixed. Consumer Discretionary was the only sector showing clear positive movement, gaining 0.34%, while Real Estate was the weakest sector, falling 4.72%. Materials, Industrials, Financials, and Communications Services also declined, reflecting cautious investor sentiment across several parts of the market.

Overall, the weekly report suggests that Bahrain’s market sentiment remained stable but selective. The headline index posted a modest gain, supported by strength in a few key names, while broader sector performance showed continued pressure in real estate, materials, and financials.

Commodities Market Update: Oil Volatility Dominates, Gold Softens

Commodities traded with a cautious tone last week, led by sharp swings in oil, gold, and industrial metals. Crude oil remained the main focus as uncertainty around U.S.–Iran peace talks and supply risks linked to the Strait of Hormuz kept energy markets volatile. Brent crude ended near $103.54 per barrel, while WTI settled around $96.60, but both benchmarks still posted weekly losses as traders balanced supply disruption fears against hopes for a diplomatic breakthrough.

Gold weakened for a second consecutive week as higher oil prices raised inflation concerns and pushed investors to price in a greater chance of tighter U.S. monetary policy. Spot gold fell to around $4,515.83 per ounce, down about 0.4% for the week, while silver, platinum, and palladium also declined.

Bitcoin remained volatile but showed a positive bias last week, trading around the $76,000–$77,000 level after recovering from weaker intraday levels.

Figure 4: Commodity and Cryptocurrency Weekly Performance

Key Takeaways for the Week

- Oil and geopolitics dominated market sentiment. Uncertainty around U.S.–Iran peace talks and supply risks near the Strait of Hormuz kept oil prices volatile and influenced inflation expectations.

- Higher yields kept investors cautious. Rising Treasury yields increased concerns that interest rates may stay elevated for longer, putting pressure on gold, growth assets, and rate-sensitive sectors.

- Regional markets stayed broadly positive. GCC and regional indices mostly ended higher, with Oman standing out as the strongest performer, while Bahrain showed stable but selective gains.

- Commodities showed mixed performance. Oil remained the key focus, gold weakened for a second week, and industrial metals stayed sensitive to supply and policy risks.

- Crypto improved but remained sentiment-driven. Bitcoin traded around the $76,000–$77,000 range, showing a positive bias, but broader crypto markets remained volatile.

FinTake View | Global, GCC & Bahrain

Global markets remained cautiously positive during the week, supported by resilient equity sentiment, but investors stayed alert to higher bond yields, inflation risks, and oil volatility. The key global driver was the interaction between geopolitical uncertainty and monetary policy expectations, which kept markets selective rather than broadly bullish.

GCC markets ended the week on a broadly positive note, helped by firm oil prices and improving regional sentiment. However, gains were uneven across the region, showing that investors are still balancing the benefits of energy strength against external risks such as global rates, inflation pressure, and geopolitical developments.

Bahrain’s market showed stable but selective performance, with the Bahrain All Share Index posting a modest gain while the Bahrain Islamic Index delivered a much stronger jump. Trading activity remained active, but sector performance was mixed, suggesting that market momentum is present, though concentrated in selected stocks rather than spread across the full market.

Sources: AP News, Reuters, Bahrain Bourse, Bureau of Labor Statistics, Federal Reserve, Dubai Financial Market, Investing.com, Investrade, Yahoo Finance, Zawya by LSEG.

Compiled & edited by: Dr. Tanvir Mahmoud Hussein, Associate Professor (Finance).